Key Takeaways

- There are 8,500 ETFs globally, and most have company overlap.

- Some ETFs are created using algorithms that include miscategorized companies.

- Actively-managed ETFs have a team of SMEs to ensure proper diversification and are more cost-effective than hiring a financial advisor.

Public markets have provided a platform for individuals to invest in stocks, bonds, and other financial instruments that can generate long-term returns. Historically, successful public market investing meant building a well-diversified portfolio that minimized risk and volatility while maximizing returns.

The popular option has been to follow the advice of late Vanguard Founder John Bogle, and buy a low-cost, passively managed total market index. In recent years, algorithms and rule-based investing have transformed public markets. This has resulted in an increase in the number of passively managed exchange-traded funds (ETFs) that include companies based on whichever algorithm a fund uses.

A Crisis of Options & Quick Turnaround

With more options than ever, we find ourselves in a situation where the same companies appear repeatedly in multiple ETFs. It’s like playing a never-ending game of “Where’s Waldo?” except instead of trying to find Waldo, everywhere you look is Waldo, as the same companies keep popping up in multiple ETFs.

The Reverse-Waldo Effect isn’t the only issue plaguing public markets. Companies are going public without rigorous due diligence, speculative funds are on the rise, and social media sentiment often drives trading activity.

In other words, the public markets have become a circus.

The next question, then, is how do we sort through the mayhem and make sound investment decisions?

“It’s like playing a never-ending game of “Where’s Waldo?”, except instead of trying to find Waldo, everywhere you look is Waldo, as the same companies keep popping up in multiple ETFs.“

The Beginning of ETFs

Let’s go way back.

The first ETF was the SPDR (Standard & Poor’s Depository Receipt), launched in 1993 by State Street Global Advisors. It tracked the S&P 500 index and quickly became a popular and cost-effective way to invest in stocks. Today, the ETF industry has over 8,500 ETFs globally with trillions of dollars in assets under management(AUM).

Fund managers today strongly advocate for ETFs, as they offer transparency, lower costs, and better tax efficiency than mutual funds.

The Rise of Non-Traditional ETFs

Today, the industry has evolved with dozens of structures, from broad-market and commodity ETFs to inverse and leverage ETFs. There are also ETFs constructed using AI/NLP algorithms to ETFs that allow fund managers to influence the underlying companies by directing proxy votes at board of director meetings.

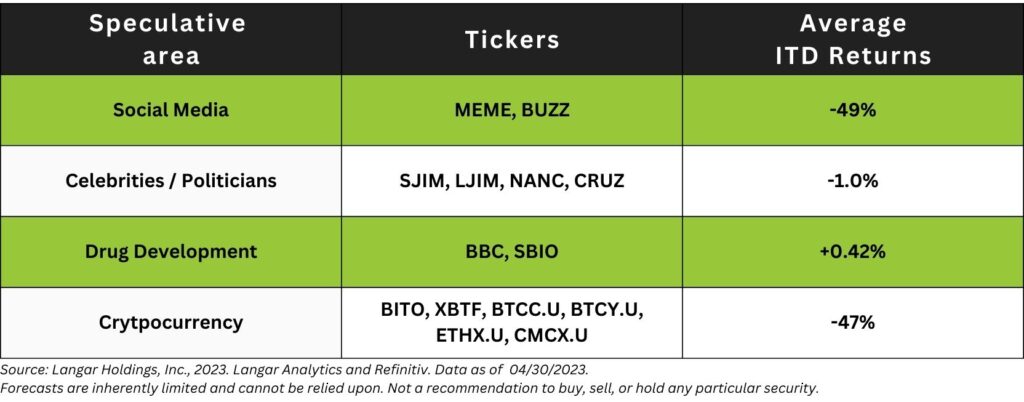

Speculative ETFs

Speculative investing refers to high-risk investments in assets with the expectation of high returns, often in a relatively short period of time. This kind of investment is typically seen through a hedge fund, run by expert fund managers, which employ teams of subject matter experts (SMEs) to continually monitor companies and their price movements to achieve above-average returns.

Full disclosure – this doesn’t always work, but a hedge fund’s limited partners (LPs) fully understand the risks and can afford to take any losses, as they are accredited investors.

Today, the problem is that we have created speculative ETFs that democratize the speculative nature of a hedge fund. Now anyone can buy into speculative strategies through these funds, but retail investors typically don’t have the excess cash reserves of an accredited investor.

Table 1* below lists some examples of different types of speculative ETFs.

According to calculations by Langar analytics, ETFs in Table 1 have a total AUM of roughly $1.5B, indicating a strong desire by retail investors to purchase speculative funds; however, with an average return of -26%, it’s clearly not a high-yielding investment thesis.

AI-Driven ETFs

As companies look to offset human labor and save money, they have relied more on AI/NLP algorithms to do the work. The problem is that these algorithms are only as good as the quality of the training data or data inputs. For public companies, there is an abundance of data in SEC filings, news articles, and social media posts, but the quality is low and when an algorithm scrapes an article, context can be lost.

“…using AI to select for companies in an ETF is like giving a participation trophy to a kid who just showed up for practice.”

For example, imagine an AI/NLP-constructed healthcare ETF that is supposed to include any company that mentions “telemedicine” in a news article. What if there is a news article that discusses a company that acquired a telemedicine company or one that put a telemedicine competitor out of business? The algorithm scrapes the article and picks up the company name but doesn’t understand that telemedicine is not central to those companies’ businesses.

Put simply, using AI to select for companies in an ETF is like giving a participation trophy to a kid who just showed up for practice.

Sector classification using AI/NLP has also become an issue, as attempting to classify a company with multiple business segments into a specific sector using an algorithm is incredibly complex. For example, we can now find real estate companies that own hospital properties to be included in Nasdaq Healthcare, even though they are real estate companies and not healthcare companies.

Activist ETFs

Activist ETFs use the collective influence of investors buying that ETF to swing voting in the board of director meetings of the companies included in the ETF. The goal is often to force social responsibility onto these companies.

While it sounds great to be able to influence companies to become more climate responsible, have proper diversity, equity, and inclusion guidelines, and/or align with religious beliefs, investors need to be aware that these principles may not result in higher returns, which is the original purpose of buying an ETF – to compound your money.

But A Total Market Index ETF is Safe, Right?

The idea is straightforward: investors can have a well-balanced and secure portfolio by owning hundreds of diverse companies. However, while a total market ETF is great for owning the S&P 500, it can fall short when buying the entire U.S. market or a sector-specific total market.

In the past, investing in the entire U.S. market made sense because the only way for a company to go public was through a rigorous due diligence process via an initial public offering (IPO). However, with the advent of direct listings and special purpose acquisition companies (SPACs), companies can now go public without undergoing the same level of scrutiny. This poses a problem because some of these companies may not be financially stable. In fact, there are currently publicly traded companies with no revenue because they haven’t yet commercialized their product. Despite this, these companies are included in the U.S. total market index simply because they are U.S. headquartered.

It’s doubtful that Bogle had these examples in mind when he encouraged diversification through index funds.

Again, it’s a circus!

Bring in Animal Wranglers Humans | Actively Managed ETFs

Like in any circus, the order is maintained by ensuring humans (or animal wranglers) are kept in the loop.

Translation: we need a human touch with ETF management, or what’s known as actively managed funds.

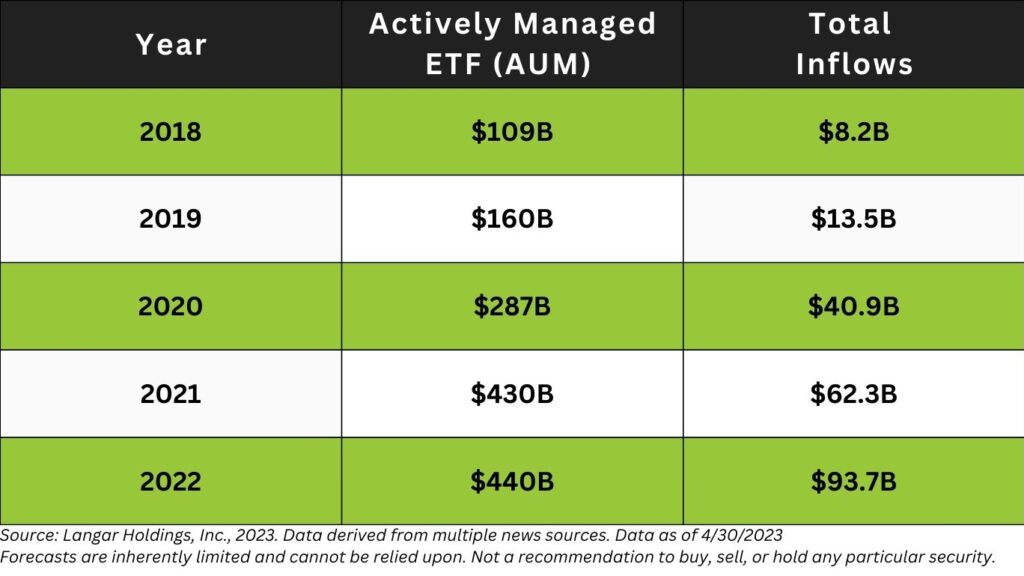

The last five years have seen a steady increase in actively managed ETFs (Table 2). Despite actively managed ETFs making up less than 5% of overall U.S. ETF assets under management, they account for 12% of the industry’s net inflows.

Actively managed ETFs are managed by professional fund managers who use a specific investment thesis (or goals) to drive investment decisions.

Examples of investment theses:

- Outperform the market

- Optimize the basket of companies for low-risk / volatility

- Only include specific companies in a specific sector that are continuously vetted by an investment committee

The investment teams for these funds usually consist of SMEs that continuously monitor the basket of companies and make trade decisions based on the most up-to-date information.

A human touch can be truly valuable in certain situations.

For instance, consider a public company whose C-suite has been indicted for fraud. While the company’s market cap could decrease by 30%, it may still meet the minimum threshold required for inclusion in a passively managed, algorithm-based ETF. In other words, retail investors will still have their money invested in a company that is no longer stable and has an uncertain future.

Actively managed ETFs could review these discrepancies and exclude the companies from the ETFs as soon as possible. This active approach provides retail investors with greater flexibility and the promise of a portfolio that is actively mitigating risk while ensuring diversification.

For anyone worried about how expensive it is to have a human at the helm, you can breathe easy. Actively managed funds have an average expense ratio of 0.7%, which is cheaper than a mutual fund’s typical fee of 1-1.5%, and below the average 1-2% fee that a financial advisor charges when managing a portfolio.

Take An Active Role in the Public Markets

The public market landscape has undergone a significant transformation due to the increasing use of computer and rule-based algorithms to create numerous passively managed ETFs with overlap.

The varying investment theses of these funds may not align with retail investor goals and may expose investors to high-risk, unstable companies in the long run.

Thankfully, actively managed ETFs offer a solution to the market’s unpredictability. By employing active management strategies, these ETFs can better navigate market fluctuations and deliver superior value.

Dhruv K. Vig, PhD

Dr. Vig is the co-founder and Chief Executive Officer of Langar Holdings. He previously worked at Silicon Valley Bank, building their global healthcare research division, and has extensive expertise and experience working with HealthTech startups.